The Most Crowded Short in the Market — and Why It Unwinds in 2026

Fat Tail Macro | February 20, 2026

The Setup

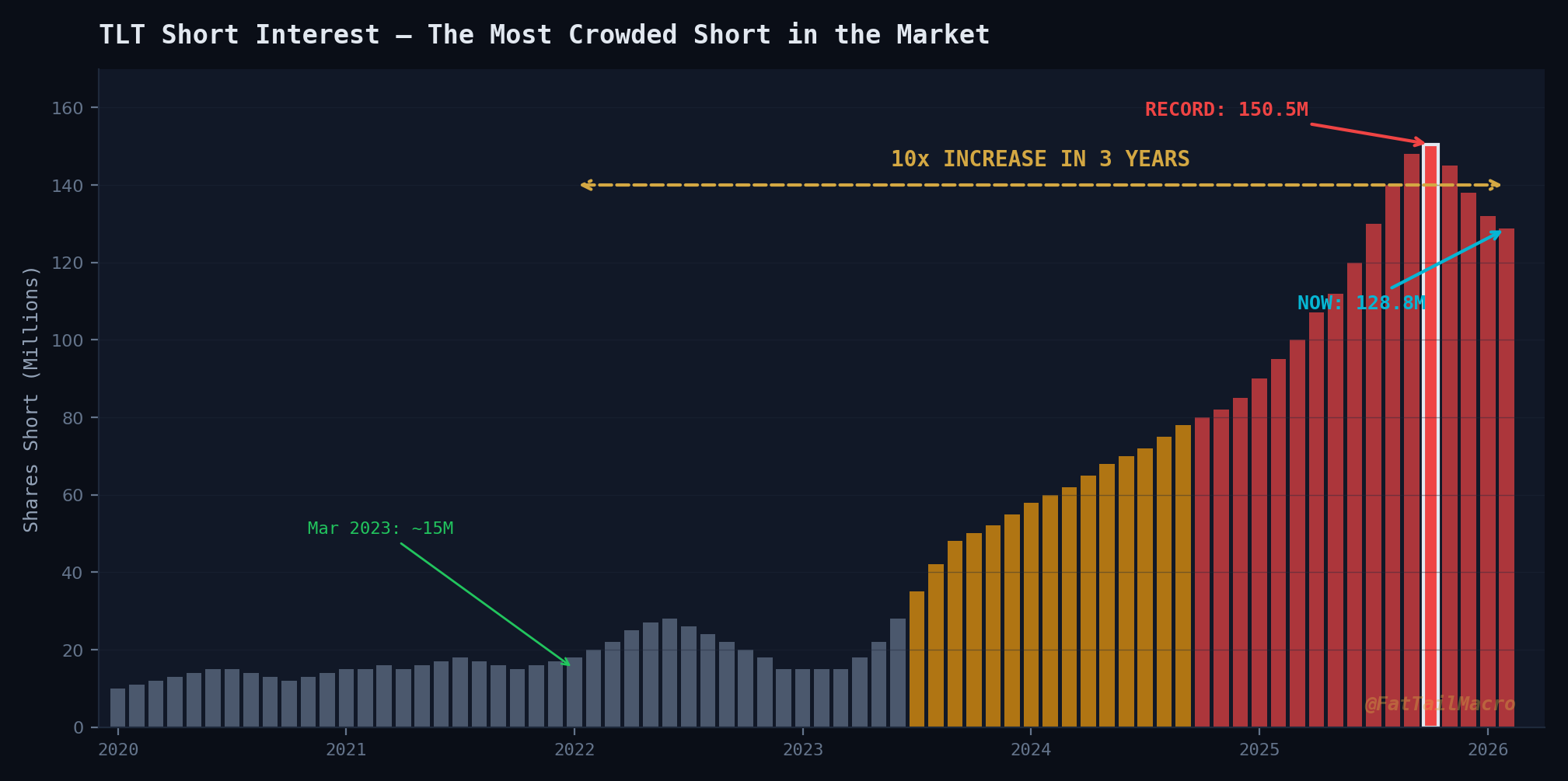

128.8 million shares of TLT are sold short right now. That’s 24% of the float — ten times the level from March 2023.

Long-term Treasuries have been in a bear market for nearly six years. Since April 2020, TLT has declined over 40%. The biggest drawdown hit -47% in October 2023. If you’ve been short bonds over that period, you’ve been handsomely rewarded. Every new short seller looked at the guy before him and saw profits.

That’s exactly how crowded trades end.

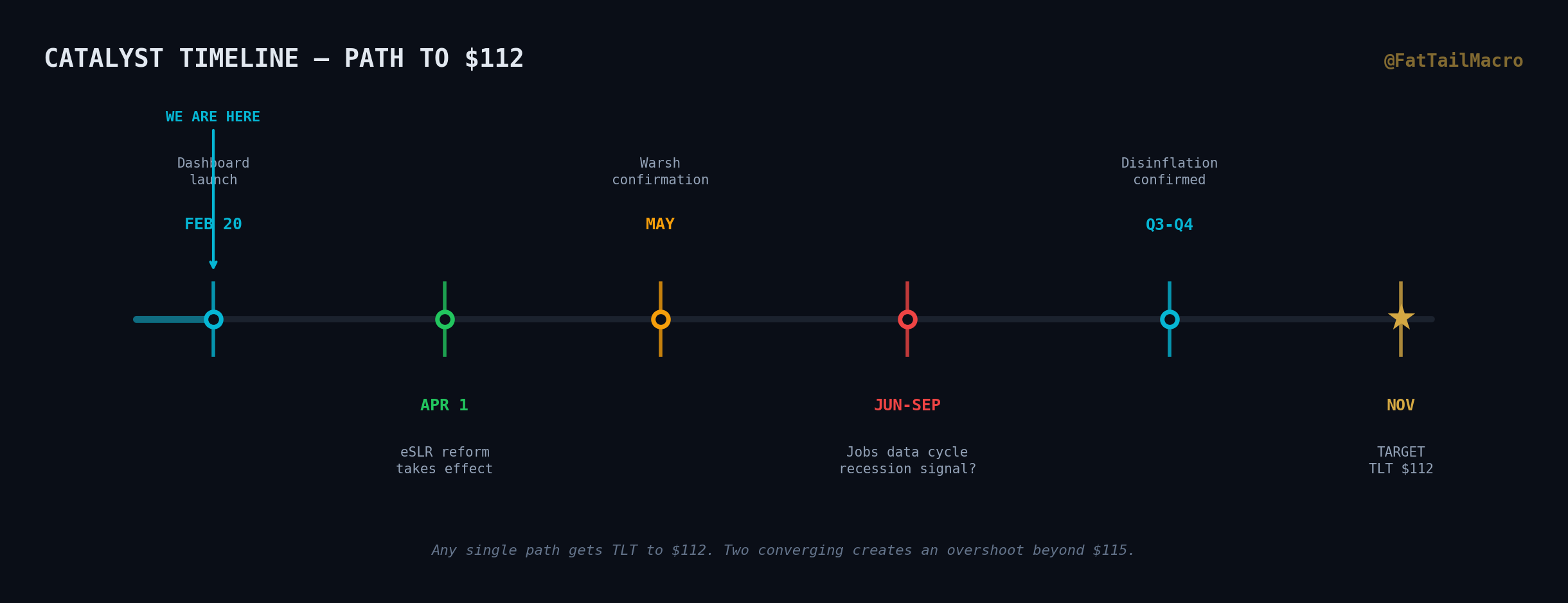

TLT sits at $89.66 as I write this. The 52-week range is $83.30 to $94.09. Consensus says we stay in this range or drift lower. I think we see $112 by November 2026. Here’s the framework.

Why the Consensus Is Wrong

This weeks FOMC minutes from the January 27-28 meeting told two stories. The headline story: a 10-2 vote to hold rates at 3.50-3.75%, with “almost all” participants backing the pause. Growth upgraded from “moderate” to “solid.” Market read: hawkish, rates stay high, move along.

The real story is buried in the details.

Two governors — Christopher Waller and Stephen Miran — dissented. They wanted a 25 basis point cut to 3.25-3.50%. That’s not a lone dove trying to make a statement. That’s two FOMC members building the foundation for a cutting campaign before Kevin Warsh even takes the chair.

Then there’s the language on tariffs. The committee characterized tariff-driven inflation as “one-time effects” that will “fade by mid-2026.” Read that again. The Fed is pre-writing its permission slip to look through inflation and cut anyway. When you tell the market that price pressures are temporary before you’ve even seen them fully materialize, you’re not describing the economy — you’re building a narrative.

The Fed staff revised UP its growth outlook, with real GDP expected above potential through 2028. Longer-term inflation expectations remain “well anchored.” Translation: the committee sees no structural reason to keep rates elevated once the tariff noise clears.

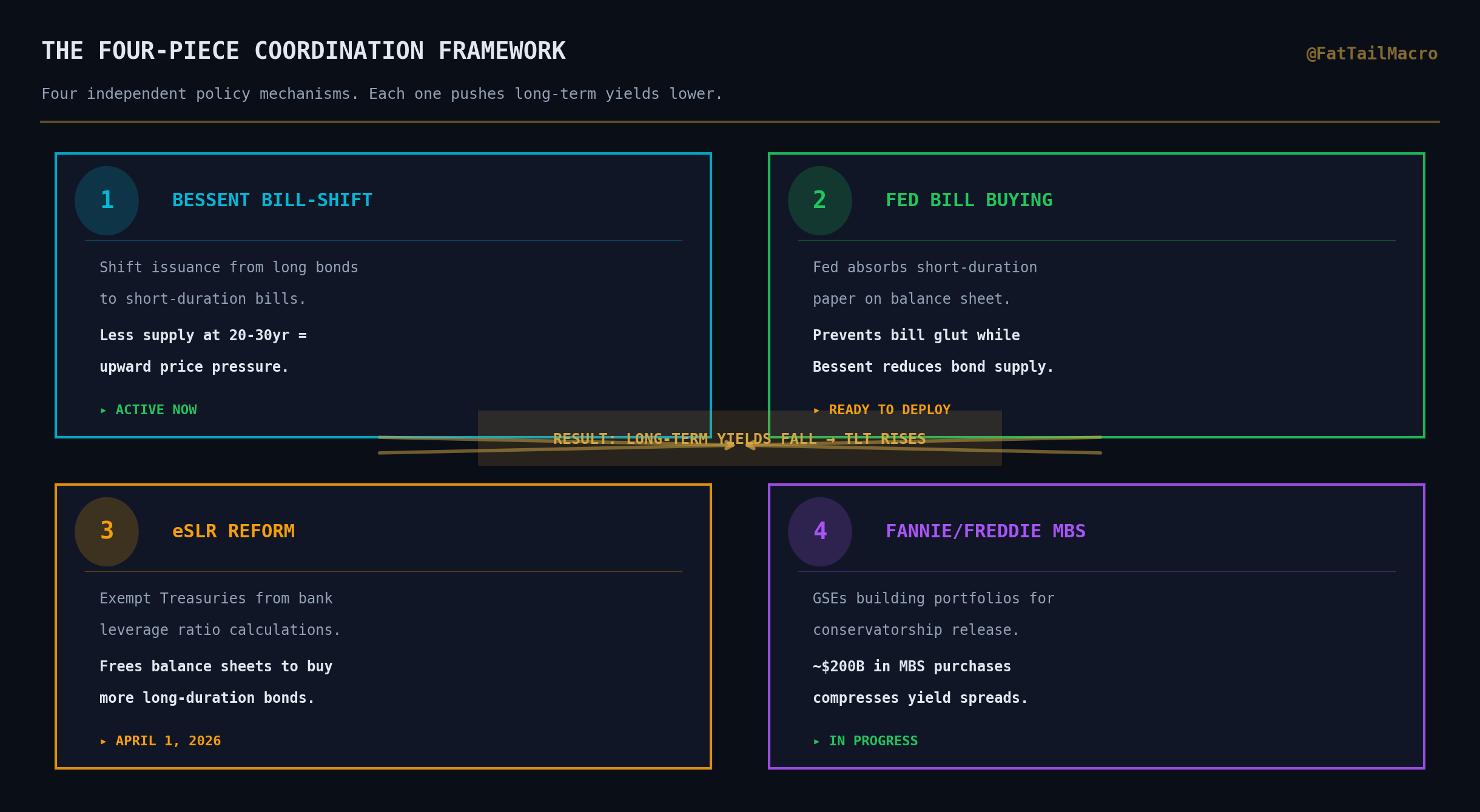

The Four-Piece Coordination Framework

This is where the thesis gets specific. I’m tracking four policy mechanisms that, individually or together, push long-term yields lower:

1. Bessent’s Bill-Shift Strategy

Treasury Secretary Bessent is actively managing the maturity profile of Treasury issuance. By shifting issuance toward shorter-duration bills and away from long-dated coupons, he reduces supply pressure on the long end. Less supply at the 20-30 year maturities = upward pressure on bond prices. This isn’t speculation — it’s observable in the quarterly refunding announcements.

2. Fed Bill Buying

The Fed can support the bill-shift by absorbing short-duration paper on its balance sheet. This keeps the bill market from getting oversaturated while Bessent reduces long-end issuance. The mechanics are straightforward: Fed buys bills, Treasury issues fewer bonds, long rates fall.

3. eSLR Reform (April 1, 2026)

This is the most underappreciated catalyst. The Supplementary Leverage Ratio (SLR) currently forces banks to hold capital against Treasury holdings as if they were risky assets. Reform would exempt Treasuries from the calculation, freeing bank balance sheets to absorb more duration. During COVID, this exemption was temporarily in place — and it worked. Re-implementing it permanently would create substantial new demand for long bonds. The April 1 effective date is on the calendar.

4. Fannie/Freddie MBS Purchases

As the GSEs prepare for potential release from conservatorship, they’re building portfolios. An estimated $200 billion in MBS purchases would directly support the mortgage market and indirectly compress long-term yields through the spread mechanism.

None of these require a recession. None require the Fed to panic. They’re administrative and regulatory tools that work regardless of the economic cycle.

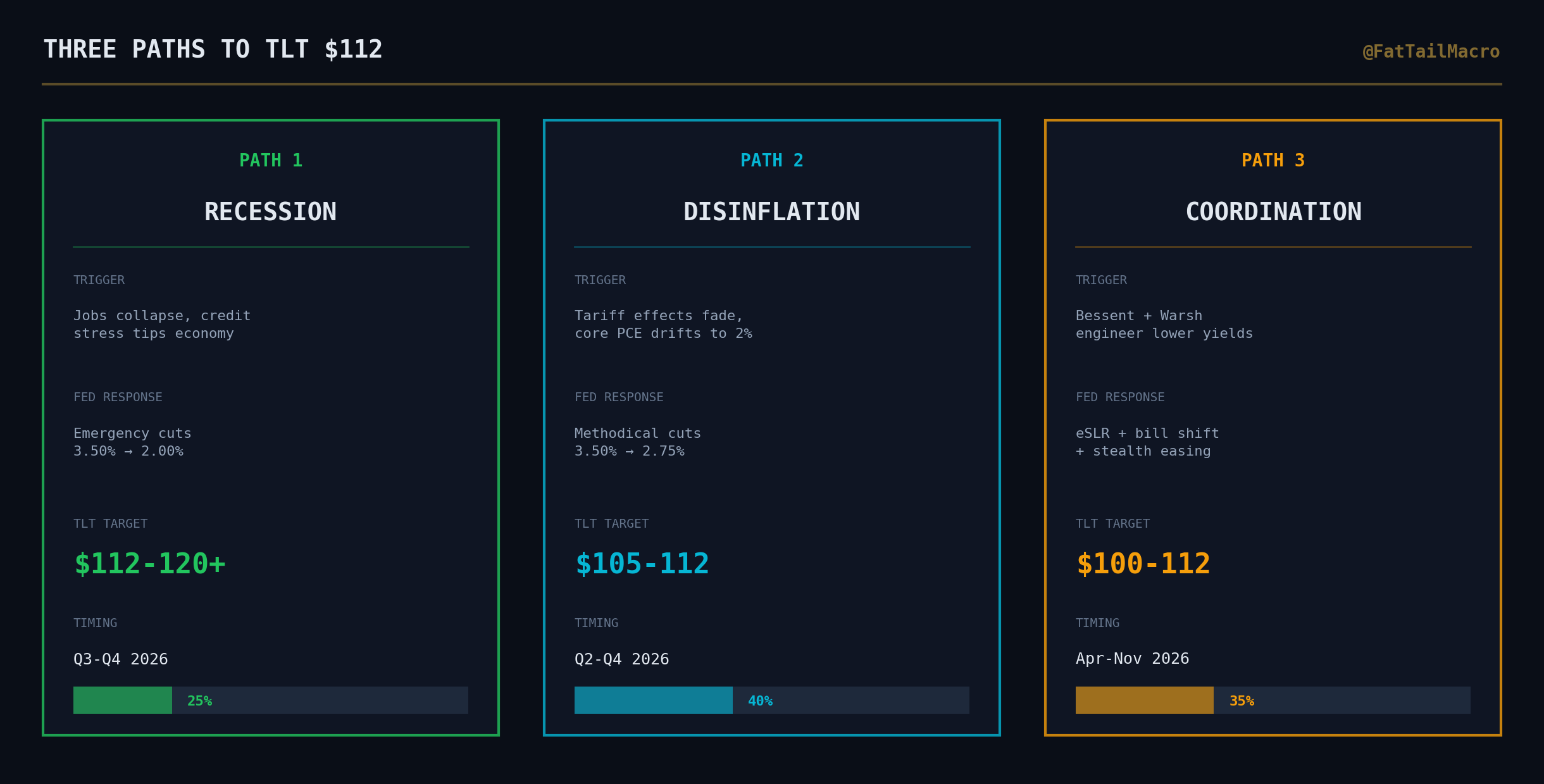

Three Paths to $112

I don’t need all four coordination mechanisms to fire simultaneously. I need one of three macro scenarios to play out:

Path 1: Recession / Jobs Collapse

The labor market is “stabilizing” per the January minutes — unemployment steady, layoffs low, but hiring subdued. That last part matters. A labor market that stops hiring doesn’t show stress in the unemployment rate until the dam breaks. If the cumulative drag from tariffs, fiscal tightening, and credit stress tips the economy into contraction, the Fed cuts aggressively. Emergency cuts send long yields to 3.5% or lower. TLT overshoots $112 easily.

Path 2: Disinflation Spiral

The committee already told us tariff effects are “one-time.” If that proves true — if core PCE drifts toward 2% by Q3 — the real rate becomes increasingly restrictive at 3.50-3.75%. The Fed cuts not because of crisis, but because the math demands it. Slow and methodical, but the direction is clear. TLT grinds to $100-105 on rate expectations alone, and the coordination tools push it the rest of the way.

Path 3: Bessent-Warsh Coordination

This is the path that nobody is modeling. Warsh gets confirmed as Fed Chair in May. He inherits a committee where two governors already wanted to cut. Bessent is already managing issuance to reduce long-end supply. eSLR reform takes effect April 1. The pieces are in place for a coordinated push to lower yields without explicit Fed easing — a “stealth stimulus” that bypasses the inflation debate entirely.

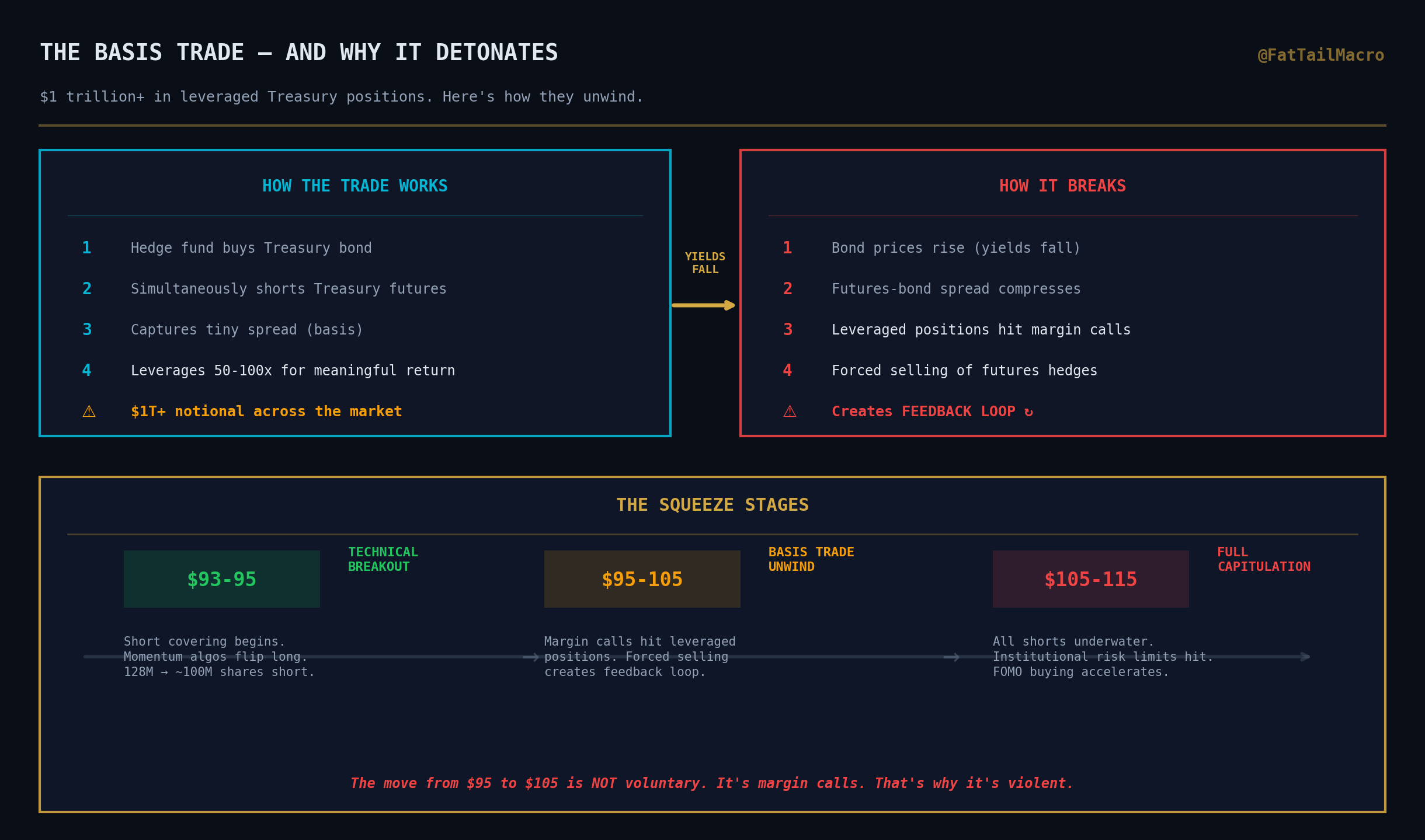

The Squeeze Mechanics

Here’s where it gets violent. 128.8 million shares short doesn’t unwind gracefully. It unwinds in stages:

Stage 1: $93-95 — Technical Breakout

TLT breaks above the 52-week high of $94.09. Technical traders cover. Momentum algorithms flip long. The move feels orderly. Short interest drops from 128M to maybe 100M. This is the “I’ll cover here and re-short higher” phase.

Stage 2: $95-105 — Basis Trade Unwind

This is the danger zone. The Treasury basis trade — where hedge funds go long Treasuries and short futures — has over $1 trillion in notional exposure. When TLT breaks through $95, the math on these trades shifts. Basis trade unwinds are not voluntary. They’re margin calls. Forced selling of futures hedges creates a feedback loop that accelerates the move. This is where “orderly” becomes “violent.”

Stage 3: $105-115 — Full Capitulation

Every remaining short is underwater. Institutional risk managers are forcing position closures. Retail piles in on the momentum. FOMO from asset allocators who missed the first 15 points. The move overshoots fair value because squeezes always do. If the $110 calls hit during this panic phase, that’s the exit — not the entry.

The Position

I hold the $110 January 2027 calls and the $100 January 2028 calls. This is a defined-risk position with asymmetric payoff.

The layering exit plan:

- Tranche 1 (25%) at TLT $95-98

- Tranche 2 (25%) at $102-105

- Tranche 3 (33%) at $108-112

- Tranche 4 (17%) at $115+ or by October 2026

If no catalyst materializes by August 2026, I begin salvaging the January 2027 calls. The January 2028 calls ride for the 2027 recession thesis.

What I’m Tracking Weekly

Every week, this dashboard updates with:

- TLT price action and key technical levels

- Short interest changes (FINRA data, biweekly)

- COT report positioning (leveraged funds, asset managers)

- Catalyst timeline progress

- FOMC statement analysis and rate probability shifts

The thesis either plays out or it doesn’t. But you’ll see the data in real time, with my positioning transparent throughout.

---

The Bottom Line

The entire market just read the FOMC minutes and concluded rates stay high forever. CME FedWatch shows 90% probability of no cut in March. First cut consensus has been pushed to July.

Everyone agrees.

That’s usually when it breaks.

*This is what I’m doing with my own money. It is not financial advice. I’m sharing my thesis and positioning publicly so you can evaluate the framework and make your own decisions. Past performance, directional accuracy, and clever-sounding narratives don’t guarantee future returns. I could be completely wrong. My options could go to zero. That’s the nature of asymmetric bets — you accept the defined loss in exchange for the undefined upside.*

Join me here and follow along on X : @FatTailMacro